Three quarters of UK life policyholders are not directing the benefits of their policies through trusts, according to Swiss Re and Insuring Change.

By failing to place life insurance in trust, more than 73% of UK life policyholders are risking the outcome of their cover.

The Life Claims: What matters most report found some progress had been made in the last year.

However, the current beneficiary gap meant the vast majority of life policies risked delays in receiving payments, potentially losing payments, or even payments ending up in the wrong hands.

In the UK, there are three main ways people can direct their life insurance pay-outs.

The first two options, using a trust or directly nominating a beneficiary in the policy, allow for a direct payment to be made to trustees or the beneficiary named in the policy.

The report explains that where the payment is simply left to an estate, it will only reach its destination after the estate has been through the probate process which can be lengthy.

In rarer cases, payment could even end up where it was not intended; for example, for cohabitees, a partner may not automatically be the recipient of the pay-out.

Furthermore, leaving the proceeds to an estate can mean it is aggregated with other assets so the estate may have an Inheritance Tax liability where it otherwise would not, depending on individual circumstances.

Minimal progress

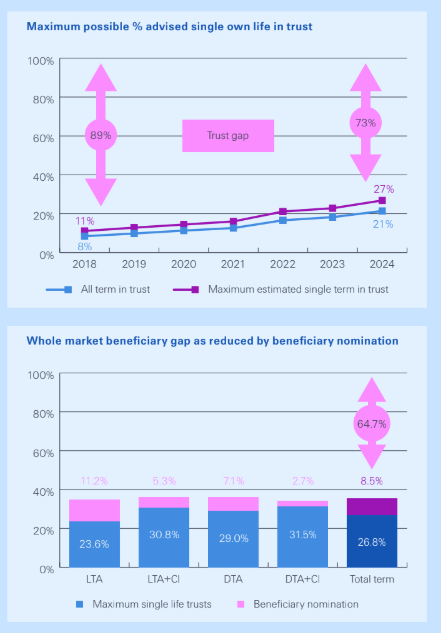

According to the report, there has been minimal progress in the last year, with policies in trust increasing 3.2% percentage points up to 21.4% of all new term plans including joint life, equivalent to 26.8% of single own life policies in 2024.

The report’s compliers note this is progress from 2018 when they estimated that 11% of new single life policies were in trust, which would imply a beneficiary gap of 89%.

However, beneficiary nomination cases have reduced the overall beneficiary gap for the market by 8.5% to a minimum of 64.7% from 73.2% if only considering trusts.

Positive signs

There were already positive signs that nominations are finding greater acceptance in the UK, with a 56.8% average uptake on nominations for products already offering this option.

With products allowing for beneficiary nomination coming to market in the UK, at the current rate of adoption the report suggested the beneficiary gap could drop to 27.7% if the whole market adopted this option.

Ron Wheatcroft, technical manager of Swiss Re Life and Health UK, (pictured) said: “Your life insurance pay-outs need to go to the people you want to benefit – quickly and with minimal stress at what is often a very difficult time both emotionally and financially.

“While it is encouraging to see another increase in the proportion of policies written in trust and in the growing use of beneficiary nominations within life policies, there is still a way to go.

“As an industry, we need to accelerate the pace of improvement.”