People buying critical illness (CI) insurance are the most likely to prize provider reputation over price when deciding on taking out cover, according to research from Royal London and Lang Cat.

CI customers were also the joint most likely to prioritise provider reputation over product cost when compared across 14 financial services products, with income protection also among this leading sector.

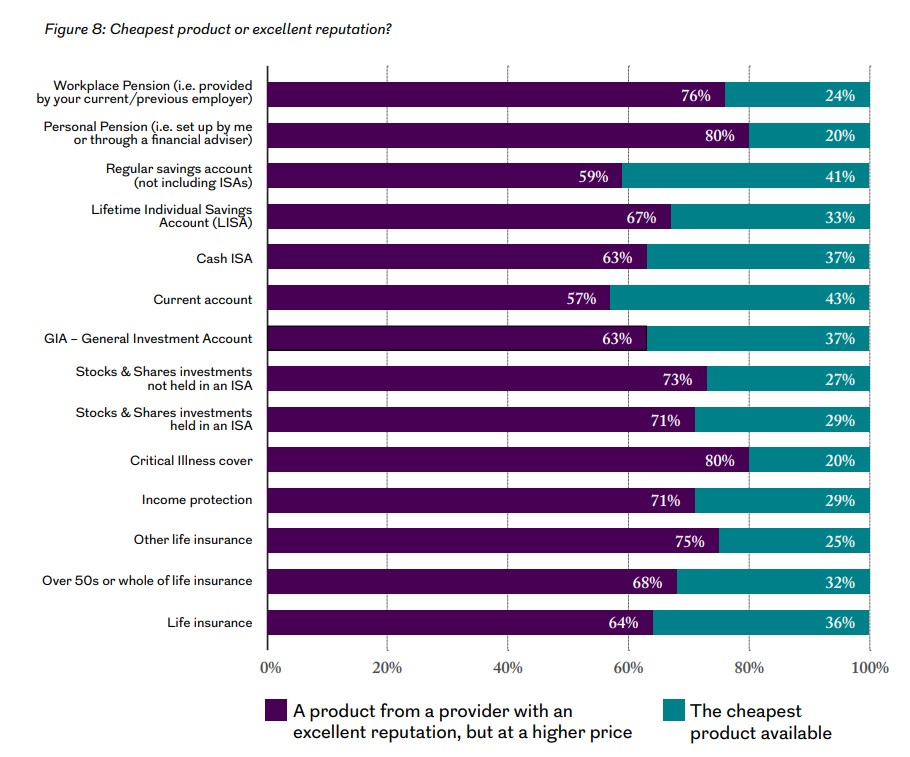

Overall, the report found across all 14 financial products surveyed that almost two thirds of customers would select the product with the good reputation at a higher price.

Those who had current accounts and regular savings accounts were most likely to be swayed by the cheapest product available at 43% and 41% respectively.

This contrasts with critical illness where this is least likely to happen, with just 20% prioritising price.

Other forms of protection cover were not far behind, with the research indicating price being the primary concern for 29% of income protection customers, 25% for other life insurance, 32% for over-50s or whole of life insurance and 36% for life insurance.

The survey of 2,000 consumers showed overall 38% had used an adviser to talk about investments, their retirement plan or arrange life insurance or a mortgage – 16% did so for a mortgage, 15% retirement, 13% investments and 9% for life insurance.

The authors said it clearly showed that value cannot be defined on price alone, with 45% of consumers defining it as a combination of getting value for money and getting their money’s worth, while only 16% defined it as price.

Responses from 160 advisers believed their clients valued peace of mind (66%), helping them reach financial goals (40%), and clear communications (38%).

The research showed that consumers did value these aspects but also placed more emphasis on positive investment returns. Half of consumers who have paid for investment advice reported that it is the most important factor for them.

When customers were asked what they valued from product providers, good communications came out top (18%), followed by customer service (11%) and security/trust (9%).

Multi-faceted and nuanced

Jamie Jenkins, director of policy at Royal London, said measuring value was more an art than a science.

“The research we have carried out with the Lang Cat has shown that different people value different things when considering products and services, and it is often multi-faceted and nuanced,“ he said.

“The temptation is to boil everything down to price because it’s more tangible, but that is only part of the value for money equation.

“If we are truly going to adopt the spirit of the Consumer Duty, then we need to develop a better understanding of what people really value. Only then can we forge a step-change in improving customer outcomes. By developing this research, we aim to start that debate.”

Mike Barrett, consulting director at the Lang Cat, added: “We hope that advisers will find this report a useful read, not only helping them to enhance their understanding of what consumers value, but also with measuring and benchmarking the value of the services they offer.

“This benchmarking exercise is not only good business sense but is now a vital part of Consumer Duty. However, the research also shows how difficult it can be for advice firms to evidence fair value.

“Value is subjective, and consumers will often combine multiple factors to make their overall value judgement. Some of these factors, such as price and investment performance are easily measurable, but other factors such as peace of mind are less tangible.

“The regulator should help advisers with good practice examples showing how these aspects should be measured under Consumer Duty.”