The Financial Conduct Authority (FCA) has launched a consultation setting new reporting requirements aimed at improving diversity and inclusion across the financial services sector.

In particular the proposals focus on boosting diversity and inclusion to support healthy work cultures, reduce groupthink and unlock talent across the sector.

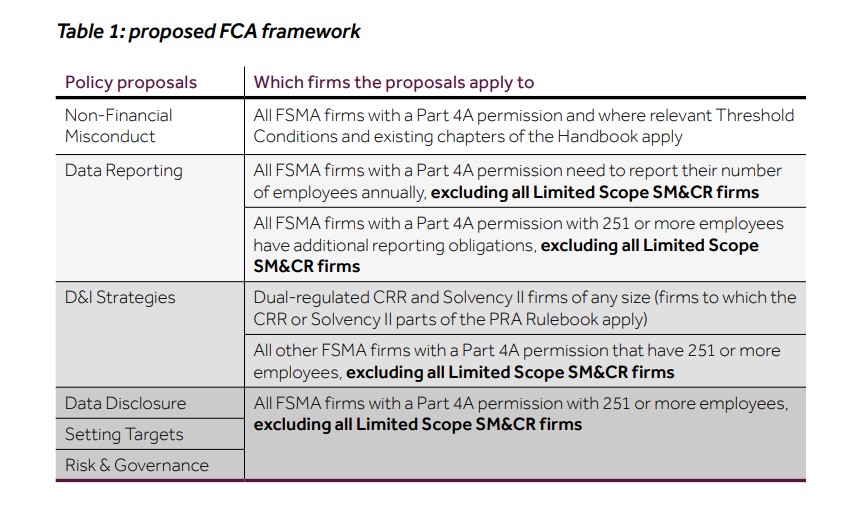

However, most of the new reporting requirements will only apply to firms with more than 250 employees.

The regulator added it also aims to “enhance the safety and soundness of firms and improve understanding of diverse consumer needs”.

This includes new rules and guidance to make clear that misconduct, such as bullying and sexual harassment, poses a risk to healthy firm culture, while the guidance will also aim to help ensure firms can take decisive and appropriate action against employees for such behaviour.

The FCA said the proposals set “flexible, proportionate minimum standards to raise the bar, placing more requirements on larger firms”.

Proposals set out for firms include requirements to:

- Develop a diversity and inclusion (D&I) strategy setting out how the firm will meet their objectives and goals;

- Better integrate non-financial misconduct (NFM) considerations into staff fitness and propriety assessments, conduct rules and the suitability criteria for firms to operate in the financial sector.

- Collect, report and disclose data against certain characteristics and set targets to address under-representation.

Under the proposals certain firms would be required to:

- Report their average number of employees to the FCA on an annual basis

- Collect, report and disclose certain D&I data

- Establish, implement and maintain a D&I strategy

- Determine and set appropriate diversity targets

- Recognise a lack of D&I as a non-financial risk

But the regulator pointed out the proposals would apply differently to firms depending on their number of employees, their categorisation under the Senior Managers and Certification Regime (SM&CR), and whether they are dual-regulated.

To reduce regulatory burden, it added smaller firms with fewer than 251 employees would be exempt from many of the requirements.

The consultation is open until 18 December 2023 with the final rules planned for publication in 2024.

Strengthening expectations

Nikhil Rathi, CEO at the FCA, (pictured) said: “For UK financial services to be competitive and for the companies in it to be well run with healthy work environments, its vital they attract, retain and promote the best talent.

“The data suggests this isn’t happening.

“Our proposals will encourage the largest firms to put in place plans and report against their delivery.

“UK financial services has long been a magnet for best-in-class talent globally. Increasing levels of diversity within firms can help attract and unlock talent, supporting the sector’s international competitiveness.

“We have taken a lead among regulators in taking a clear stance that non-financial misconduct, such as sexual harassment, is misconduct for regulatory purposes. We’re strengthening our expectations on how the firms we regulate consider such misconduct when deciding whether someone is fit and proper to work within the industry.”

Guarding against groupthink

Sam Woods, CEO of the Prudential Regulatory Authority, added: “Diversity and inclusion play an important role in guarding against groupthink within firms.

“Firms in which a broad range of perspectives is welcomed and encouraged will manage their risks better, advancing the PRA’s objective of safety and soundness.

“Stronger diversity and inclusiveness should also make firms more competitive by enabling them to attract a wider pool of talent.

“We are tabling proposals today which we think will advance our objectives, alongside existing core parts of our regime such as capital and liquidity requirements, and we welcome views on them from all stakeholders.”