A total of £2.22bn from 30,932 claims was paid out by the group risk industry during 2021, an increase of £208.4m on 2020 figures, according to data from trade body Grid.

This total includes 10,696 group income protection (GIP) claims which were already in payment and continued though last year.

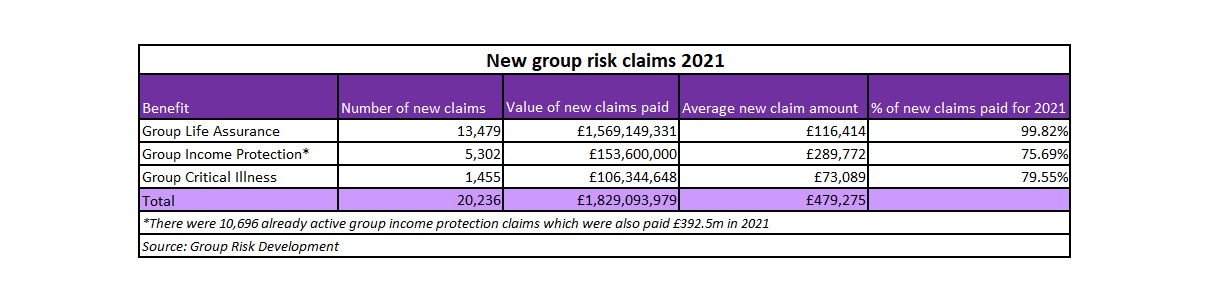

Overall, there were 20,236 new claims made in 2021 with a total of payment of £1.83bn, while the body added that 6,113 employees were helped back to work and there were 220,886 interactions with additional support services offered by insurers.

Product data

Group life assurance policies paid out £1.57bn in benefits, an increase of £198m on 2020, with an average new claim value of £116,414, while 99.82% of all claims were paid.

During 2021 there were 5,302 new GIP claims, totalling £153.6m per year and averaging £28,977 per year, with 76% of new claims approved.

When including claims already in payment, the overall total of £546.1m in GIP benefit paid was down £4.72m compared with 2020.

Meanwhile, group critical illness (CI) policies paid out benefits totalling £106.3m, up £14.7m on 2020, with an average claim value of £73,089 and 80% of claims being approved.

Cancer was the main cause of claim across all three group risk products during 2021 – responsible for 335 of life claims, 27% of GIP claims and 67% of CI claims.

Heart disease (16%), mental illness (18%) and heart attack (9%) were the second most common claims reasons across the three products respectively.

Return to work and add-on services

Grid noted that it has also captured details of cases where GIP supported a return to work with active early intervention before the employee was eligible for a monetary payment.

It found 4,395 people accounting for 45.3% of all claims submitted, (up 13.5% compared to 2020) were able to go back to work during 2021 because of such early intervention.

Overcoming mental illness (54%) and musculoskeletal conditions (10%) were the main reasons for support given.

And of the new GIP claims that went into payment during 2020, a further 1,718 people were helped by the insurer to make a full return to work by the end of 2021.

In total, there were 220,886 customer interactions during 2021 with additional help and support services funded by group risk insurers.

Of these interactions, 39% involved access to counselling, 11% were related to illness and 4% to legal issues.

Covid-19

Covid-19 had a significant impact on the group risk industry last year.

It was the third most common cause of claim on group life assurance (11.7%), with data published earlier this year showing insurers paid out more than £168m, up from £93m in 2020, with an average lump sum payment of £100,387.

In all there were 1,578 lump sum death benefit claims, plus the capitalised value of 24 dependants’ pension claims.

For group income protection, Covid was the fifth most common reason for claims.

There were 372 new claims in 2021, of which 66 had returned to work by the end of the year. This shows a pattern of increase, as there were 41 Covid-19 claims in 2020.

Declined claims

Grid also gave details on why claims were declined for GIP and CI products.

For GIP, the vast majority of declined cases was because the employee did not meet the definition of disability under the policy terms, i.e. they were still capable of doing their own job despite their reason for absence.

The body said an example of this would be someone unable to work because of caring responsibilities but not being ill themselves.

Or where medical evidence does not support that someone’s medical condition is severe enough to prevent them being able to perform the duties normally required for their job or suitably modified duties made as “reasonable adjustments” under the Equality Act 2010.

For CI, the main reason for turning down claims was the employee’s condition not meeting the definition, for example, someone claiming for a heart attack when they had only had angina.

Katharine Moxham, spokesperson for Grid, (pictured) said: “The statistics categorically show that group risk benefits really are some of the most valued benefits that employers can offer: financially, practically and emotionally.

“The figures show the extent of the holistic support offered via group risk benefits: in the event of death, serious illness, prevention, early intervention and rehabilitation

“It’s no wonder that an increasing number of employers are offering these to their workforces, and not just among large corporates, but SME and micro-SMEs too.

“Covid isn’t going away, so the support available within group risk benefits will be good news to many employers who are continually looking at ways of how to offer support as we learn to live with the virus.”