Guardian has revealed it will be expanding its product range in the coming weeks with the launch of new lower-cost life cover Life Essentials.

The launch will offer Guardian customers a choice between Life Protection – Guardian’s existing premier life cover for clients whose priority is quality, and Life Essentials – the new low-cost life cover for clients whose priority is price. Both products will be available within Guardian’s menu

In offering this choice, Guardian said it is seeking to better meet the needs of a wider range of clients, including those who have been affected by the higher cost-of-living.

It added it also expects to appeal to clients whose primary focus is affordability, for example first-time buyers, as well as clients who place less value on a feature-rich product.

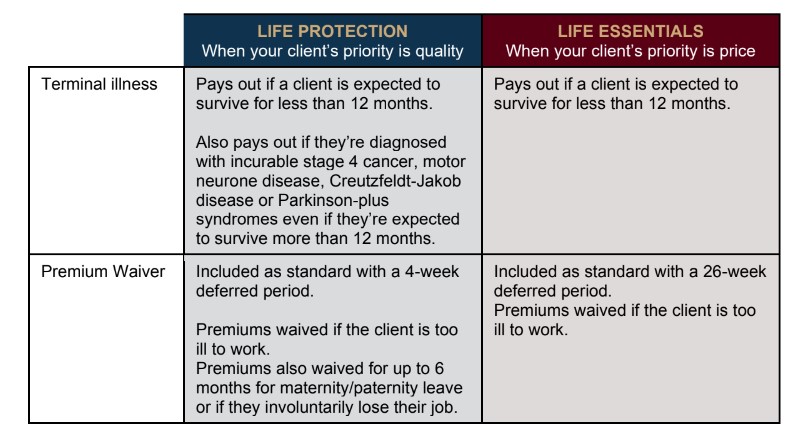

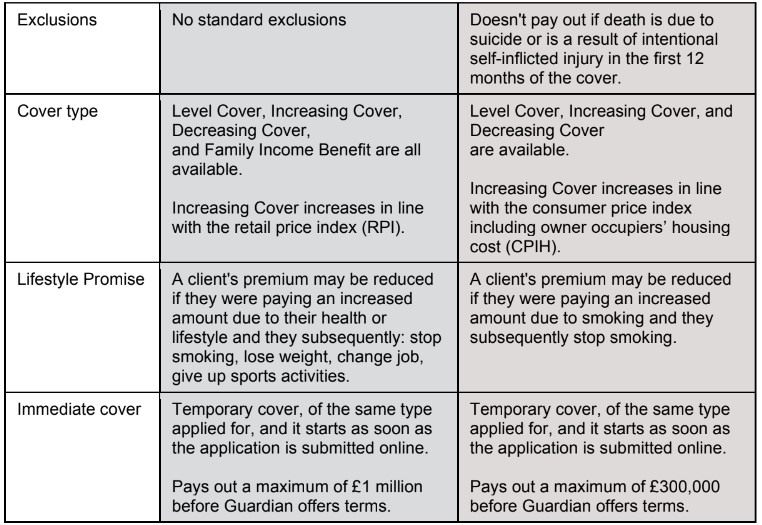

Guardian’s two life covers – Life Protection and Life Essentials

Guardian points out that the new low-cost Life Essentials cover will have many of the benefits expected from a Guardian policy.

This includes a dual life approach, Premium Waiver (with a 26-week deferred period which pays out on ‘own job’), optional Children’s Critical Illness Protection, beneficiary nomination through Payout Planner, no compromise on Guardian’s 5-star service, the same underwriting philosophy, and the same value-added services including the recently strengthened Guardian Anytime, and HALO, the protection company’s bespoke claims support service.

However, to make the product affordable, some high-quality features are reduced for Life Essentials. A full comparison of the differences between the two life cover choices is outlined below.

In particular Life Essentials has a different terminal illness definition to Life Protection.

In Guardian’s new low-cost cover, this is defined as: ‘being terminally ill and, in the opinion of the customer’s attending UK consultant, their illness has no known cure or has progressed to the point where it cannot be cured and is expected to lead to their death within 12 months’.

This contrasts with the enhanced terminal illness definition on Life Protection which does not require the 12-month prognosis for incurable stage-4 cancer, motor neurone disease, Creutzfeldt-Jakob disease or Parkinson-plus syndromes.

For both Life Essentials and Life Protection, the policy terms and conditions state that Guardian will pay out on the definite diagnosis of the policyholder’s treating UK Consultant.

Jacqui Gillies, marketing and proposition director at Guardian, (pictured) said: “We’re delighted to announce we’ll soon be offering a choice of life covers, enabling advisers and their clients to select between our low-cost Life Essentials and our existing premier Life Protection.

“The time is right to be offering this choice; the higher cost-of-living means that many clients simply have less budget available for protection. It also broadens our appeal within client segments traditionally focused on affordability, helping us reach a wider market and accelerating our distribution growth.

“We’re committed to fair value and that’s why many of the features we’re known for remain in our low cost option, including our dual life approach, Premium Waiver, Payout Planner, Guardian Anytime and HALO.

“But as you’d expect there are also some important differences, most noticeably to the terminal illness definition, which we’ve aligned with the standard market definition to keep the cost affordable for more people.”

“We believe that by offering this choice we’re supporting advisers to better meet the needs of a wider spectrum of clients – so whether their priority is quality or price, we now have a life cover to suit both.”