Axa has blamed higher health claims frequency in the UK as one of the primary factors behind an 8% decline in life and health earnings for 2023.

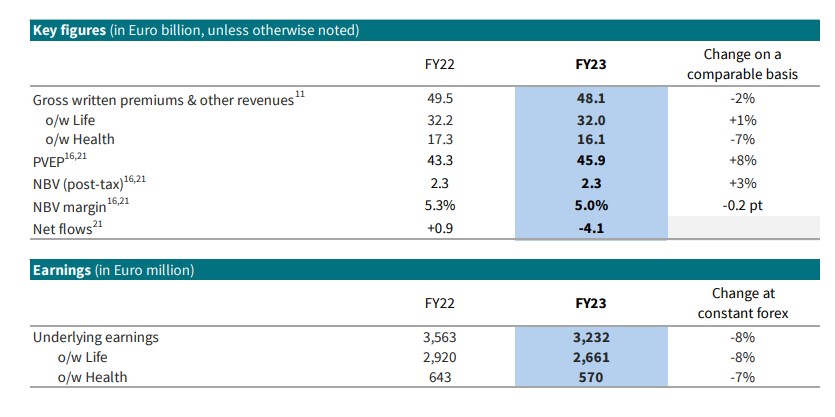

The insurer’s full year results also revealed gross written premiums and other revenues across its life and health business segment of €48.1bn which was down by 2% on the previous year.

It was not a completely negative picture, however, as despite the overall decline, life premiums climbed by 1%. That increase was mainly driven by higher sales of capital-light savings products (up by 12%), including the continued success of Eurocroissance in France which was up by 54%.

There were also higher revenues in protection which was up by 4%, notably in Japan, Hong Kong, Belgium, and Switzerland.

This was partly offset by lower sales of traditional G/A products, down by 12% in line with the group’s strategy. And unit-linked sales were also down by 11%, notably in Italy and France.

But health premiums fell by 7%, following the non-renewal of two large legacy international group contracts in France.

Excluding the impact of those contracts, Axa reported that health premiums actually increased by 7%, with continued growth across most locations primarily due to favourable price effects.

Present value of expected premiums (PVEP) was up by 8% to €45.9bn, in the life segment.

That was mainly driven by higher volumes in protection which was up by 16%, notably in Hong Kong from higher mainland Chinese visitors’ business.

New business value (NBV) was up 3% after tax to €2.3bn. Other NBV excluding new business contractual service margin (NB CSM) was up by 15% before tax to €0.8bn, mainly due to higher volumes in group protection in France.

But the NBV margin decreased to 5.0%, mainly due to protection, which was driven by a less favourable business mix.

Net flows amounted to -€4.1b, reflecting outflows in traditional G/A across most markets, which were in line with the group’s strategy. That compared to 2022, when net flows were up by €0.9b.

The negative net flows for 2023 were partly offset by protection which was up by €3.7b, mostly in Hong Kong, Japan, and France. Health was also up by €1.8b, mainly in Germany, Japan, and Hong Kong.

Life and health underlying earnings fell by 8% to €3.2b, which the insurer maintained reflected lower technical profitability in life mainly due to unfavourable prior years reserve development on a run-off portfolio in protection.

It was a similar case for health due largely to higher claims frequency in the UK. That was despite the non-repeat of elevated Covid-19 claims in Japan and am unfavourable claims experience on two large international contracts at AXA France.

Thomas Buberl, Axa CEO said “AXA reported strong results in 2023, reflecting continued execution of its strategy.

“This also marks the completion of our “Driving Progress 2023” plan. The Group has successfully delivered on all its main financial targets, with underlying earnings per share growing 9%, cumulative cash remittance of €16.4b, and return on equity of 14.9%., while maintaining a strong Solvency II ratio10 at 227%.

“In 2023, we continued to see good growth momentum in our core businesses including P&C, protection, capital light G/A savings and health.

“This was partly offset by lower volumes in AXA XL reinsurance from a reduction in property catastrophe exposure, and in health following our decision not to renew two legacy international group contracts.

“The Group reported €7.6b in underlying earnings, reflecting a strong operational performance in P&C, in particular at AXA XL.”