Sales of new long-term individual protection policies in 2023 fell 5.5% in 2023 as the cost of living crisis continued its stranglehold on households across the country.

Swiss Re’s Term & Health Watch 2024 Report revealed in 2023, a total of 1,997,450 new term assurance, whole life, critical illness, and income protection policies were purchased.

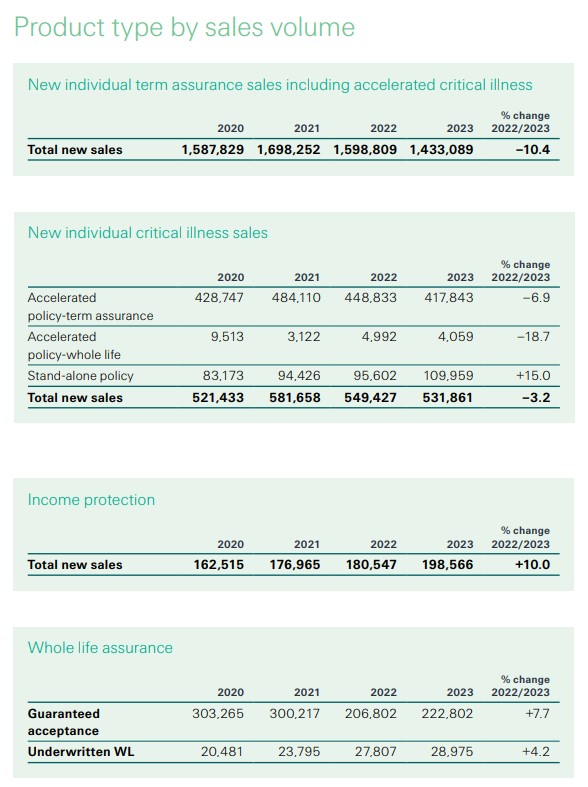

This continued the decline reported in the 2022 report when sales fell by 7.8%.

Breaking down sales by product category across term life and critical illness, all new term policy numbers fell, with the exception of relevant life cover which grew by 11.4% to 24,838.

The biggest drop in policy sales witnessed in level term without critical illness which fell by 12.3%, with a decline of more than 92,000 policies compared to 2022.

However, standalone critical illness sales bucked this downward trend, increasing by 15%.

Income protection (IP) sales increased by 10% to 198,566 driven by strong growth in to retirement age products and two-year limited payment term products, which grew by 12.5% and 12.2% respectively.

But this growth was offset by a 17.3% fall in the sale of one-year limited payment term products.

And finally, across whole of life, new guaranteed acceptance whole life purchases increased by 7.8%.

While new purchases remain low compared with 2021 and before, sales of underwritten whole life policies rose by 4.2% to 28,975 policies.

Provider rankings

While Legal & General continued to be the top provider measured by the number of new term assurance sales with and without critical illness (312,591), Aviva overtook L&G for new critical illness sales (112,606) and new income protection sales (54,900).

In premium, Legal & General ranked top among product providers with and without CI (£116,737,446) as well as among providers measured by premium for new income protection sales (£23,703,331).

For new guaranteed acceptance whole life sales SunLife topped the list of product providers completing 130,559.

Another challenging year for households

According to Joanna Scott, author of Term & Health Watch 2023, and technical manager and industry affairs manager, L&H UKI, at Swiss Re, the findings reflect another challenging year for UK households, with rising interest and mortgages rates compounding financial pressures and resulting in a slowing housing market.

Scott said: “It is great to see that income protection sales continue to grow at a good pace.

“The numbers seen in Term & Health Watch build on the strong workplace long-term disability insurance numbers we reported in our Group Watch report earlier this year.

“However, as higher interest rates persist, it is no surprise that new term purchases suffered as the pressure on households continues.

“There is also still a huge gap where UK workers would receive little to no support if they were to fall ill.

“Many employees do not enjoy cover which goes beyond statutory sick pay (SSP) at £96.35 a week and there are 4.26 million self-employed workers in the UK who have no entitlement to SSP.

“So while we are encouraged by the growth in income protection sales, there is more to be done to raise awareness across the industry to those who would still be exposed if the worst were to happen.”

Ron Wheatcroft, technical manager at Swiss Re, (pictured) added: “The fall in the number of new non-advised term products shows that the cost of living continues to impact people’s willingness to seek out life cover when faced with other competing priorities.

“The difficult mortgage market has affected decreasing term assurance sales, both with and without a critical illness benefit, but it is good to see new critical illness purchases outside the mortgage sector faring much better by comparison.

“As before, the results show the value that a good adviser can bring, such as the opportunity to build on and foster an existing customer relationship.

“Swiss Re data also show that higher numbers of policies are placed in trust through advised channels, which provides peace of mind that the proceeds of the policy will go to the right beneficiaries.”