Individual protection insurance sales in the UK fell by 7.8% in 2022 – reversing the rebound the market experienced in 2021, according to Swiss Re’s latest Term & Health Watch report.

The economy may now be recovering from Covid, but indications are that 2023 might not be much better than 2022.

Looking at the first quarter of this year, the report’s compilers indicated a slower start for the market than in 2022. Advised protection business for the period tracked marginally below sales last year by 3%. But on the plus side, the premium value of business written was up by 9%.

According to the report’s compliers, 2022 was a year characterised by uncertainty and political change, intensified by high inflation and an escalating cost-of-living crisis, negatively impacting sales.

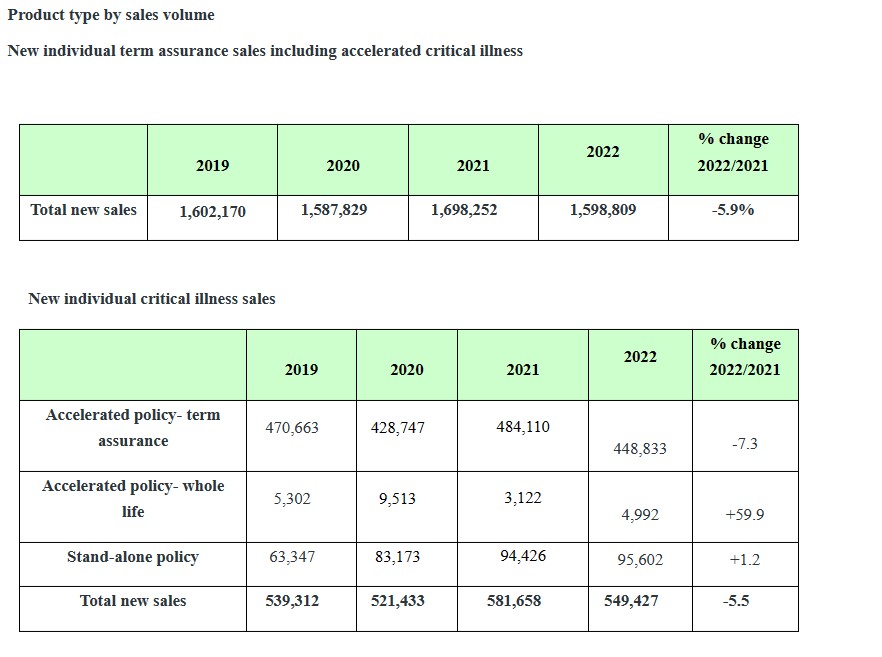

The 2022 report, produced in conjunction with IPipeline, found that a total 2,114,559 new term, whole life, critical illness, and income protection policies were sold in 2022 – down 7.8% on 2021.

This compared with the 2,293,704 new term assurance, whole life, critical illness and income protection policies which were purchased in 2021, up from 2,157,263 in 2020 – an increase of 6.3%.

With the outset of Covid in 2020, individual protection policy sales for that year had declined by 1.2%, representing the first fall since 2013.

Joanna Scott, author of Term & Health Watch 2023 and technical manager and industry affairs manager life and health UK and Ireland, at Swiss Re, said “the cost of living crisis will have impacted households differently depending on their overall financial resilience.

“However, most people will have felt the impact of inflation in the last 12 months, so it is unsurprising that individual long-term life and health protection sales were impacted.”

Delving deeper into each product category, total new term assurance sales in 2022 fell by 5.9% from 1,698,252 to 1,598,809 in 2022.

The number of term assurance-only new policies was also down 5.3% to 1,149,976. While there was a drop in new sales for term and critical illness overall, there was a rise in average new sums assured and premiums for all term assurance and critical illness products.

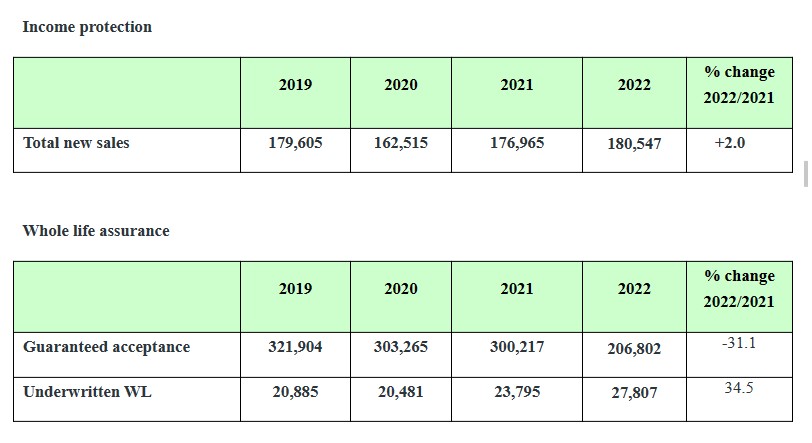

The picture wasn’t all bleak, as total underwritten whole life sales increased by 34.5% to 27,807 policies. The report’s compilers attribute this partly to a reaction to the government’s decision to freeze the UK’s Inheritance Tax thresholds once again.

But total guaranteed acceptance whole life sales were 206,802, down 31.1%.

However, the total number of new individual income protection policies sold rose by 2% to reach 180,547. Total income protection premiums increased by 12% in 2022.

New maximum two-year benefit payment policies exceeded the number of “to retirement” income protection policies sold for the first time (86,309 and 78,397 policies respectively).

Legal & General retained its position as the top provider measured by the number of new term assurance sales with and without critical illness (440,723), for new critical illness sales (119,624) and new income protection sales (49,456).

Canada Life’s withdrawal from the market in November 2022 and by Aegon in April this year will be covered in next year’s numbers given the timing of these announcements.

“It was a challenging year for total new sales compared to 2021, but it was encouraging to see that average sums assured had increased” Scott continued.

“With the Covid-19 pandemic and resulting bounce back, we are now back to the numbers we saw in 2019. We would ideally want to see growth; but, considering the economic environment we experienced last year, the market may be more robust than anticipated.

“It is positive that people continue to look to protect themselves against shocks.“

Ron Wheatcroft, technical manager life and health UK and Ireland, at Swiss Re, (pictured) added that the decline in new level term non-advised purchases was one of the stand-out statistics this year, with 42% of total sales still “well ahead” of the 24% seen in 2018 but “way below” the 50% in 2021.

“New level term non-advised sales fell by 24% and those with a CI benefit by 27%,” Wheatcroft continued.

“The market faced some difficult challenges, and we attribute this fall in part to the cost of living crisis which has put people off making what they may see as discretionary purchases.

“Above inflation new sums assured for level term in particular (11.7%) reflect that advisers appear to be managing better in the current difficult environment.”