Mortgage Advice Bureau (MAB) saw its protection revenue increase by more than 13% in 2025 to break the £100m mark with sales up 7%.

The national mortgage and protection intermediary earned £102.7m in pure protection commission last year, up 13.5% from £90.5m in 2024.

This came with a 7% increase in the number of protection policies sold to 99,500 from 93,400, and a 29% rise in protection-only advisers to 182 from 141.

In its annual results MAB noted it was increasingly reviewing protection needs away from mortgage events as the firm continued to invest in the market.

The firm also welcomed the Financial Conduct Authority’s (FCA) interim report of its pure protection market review, particularly the finding that loaded premiums and restricted panels were not creating worse pricing outcomes.

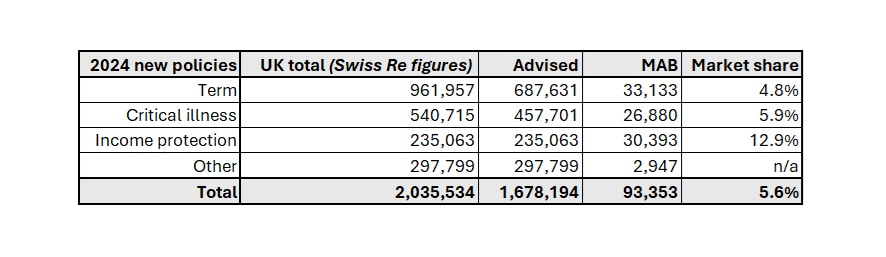

Using the most recent industry data available, MAB said it accounted for 5.6% of all advised pure protection sales made in 2024. (see table)

This rose to more than one in ten for income protection (IP) new business.

“Pure protection commission revenue increased by 13% year on year,” the firm said.

“Growth reflected an increase in policy volumes and a modest increase in average premiums. The protection mix remained broadly unchanged between 2024 and 2025.

“Performance also benefited from continued investment in protection capability, including the expansion of our team of dedicated protection advisers operating alongside our core mortgage proposition.”

It added that growing protection revenue remained “a key pillar of the group’s strategy, and our investment in this area is expected to support further growth in the coming years”.

‘Strategic growth priority’

The intermediary firm emphasised that protection remained a strategic growth priority for it, with increasing focus on engagement beyond the mortgage event.

It noted that regulatory momentum had been constructive in the protection market, highlighted by the FCA’s Pure Protection Market Study interim report which recognised many positive elements including high claims acceptance rates and that it does not envisage significant market interventions.

“The FCA also notes that, on average, practices such as loaded premiums or restricted panels are not creating worse pricing outcomes, aligning with MAB’s long-standing approach to panel governance and fair value,” it said.

“MAB welcomes these findings and remains committed to maintaining the highest standards of consumer outcomes and regulatory engagement, while supporting the continued development of the protection market and the reduction of the protection gap.”

MAB also noted that its protection engagement was now supported by a standalone, data-led nurture programme, with reviews decoupled from the mortgage event.

“This process is already driving higher customer engagement and is expected to strengthen long-term relationships and improve outcomes across the full customer lifecycle,” it said.

“It will also begin to eliminate historical variance in attachment rates based on whether the transaction is a purchase, a remortgage, or a product transfer.

“Looking ahead, we expect growth in 2026-27 to be led by the refinance and protection segments.”

Income up, profit slips

Despite the growth in commission, insurance slipped to 37% of MAB’s £318.8m revenue as mortgage procuration fees surged 27% to more than £133.9m, up from £105.8m.

Overall, MAB’s profit after tax for 2025 slipped 4.5% to £15.4m from £16.1m, however founder and chief executive Peter Brodnicki was upbeat about the figures.

“Despite the current geopolitical environment, the structural opportunity remains compelling. Around two-thirds of UK mortgage transactions are refinancing, which continue regardless of economic conditions,” he said.

“At the same time, the UK faces a well-documented protection gap, recently highlighted by the regulator, which represents a significant long-term opportunity for high-quality advice.

“Increasingly, protection needs are being reviewed outside the mortgage event, creating an additional and growing source of recurring revenue for MAB.”

Brodnicki also highlighted that the firm was building new strategic partnerships and pursuing selective mergers and acquisitions to expand its role in the home-moving process, widen the proposition and add value to customers ahead of upcoming government changes to the home-buying and selling process.

“Engaging customers earlier in their research journey and broadening our B2C proposition will further strengthen our ability to capture, convert and support customers through every stage of homeownership,” he continued.

“Through continued organic growth, disciplined acquisitions and the increasing use of technology, data and AI, we believe MAB is well positioned not just to participate in the mortgage market, but to shape where it goes next.”