Private medical insurance (PMI) funded hospital admissions hit another record high in 2025 after bouncing back in the final quarter of the year.

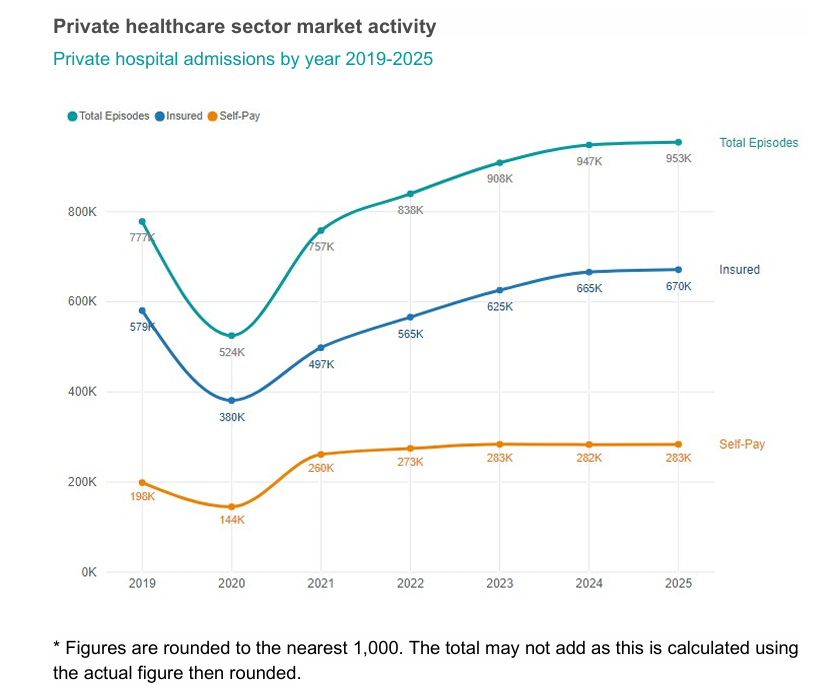

There were 670,000 insurance-funded hospital admissions last year, up by more than 5,000 from 665,000 in 2024, which itself had been a record figure.

The final three months of the year saw PMI-based admissions up by 8,000 when compared with the corresponding quarter of 2024.

Private Healthcare Information Network (PHIN) data showed 168,000 hospital admissions through private medical insurance (PMI) in October to December 2025, up from 162,000 in July to August 2025.

Record admissions

More broadly, the total number of UK private-funded hospital admissions in 2025 was 953,000 which was 1% up on 2024 – meaning the private sector had more admissions than in any previous year on record for the fourth year in a row.

Three out of four quarters in 2025 witnessed a record number of admissions. The remaining quarter was only beaten twice before.

In 2025, the largest percentage growth by nation occurred in Scotland (6% or 3,045 admissions) followed by Wales (1.8% or 570 admissions). While there was smaller percentage growth in England (0.4%) it saw the highest growth by volume, up by 3,545 admissions.

However, the number of private admissions fell in Northern Ireland by 4.8% or 1,135 admissions.

Record levels of insured activity

Looking at the past year as a whole for insured admissions, Q1 2025 was the highest quarter ever for admissions (174,920) paid for with private medical insurance.

Furthermore, Q3 and Q4 2025 also saw higher admissions than in the equivalent periods in 2024. Only Q2 was lower, but this was still above all years pre-2024.

In total, there were 6,485 more insured admissions in 2025 than in 2024 – a 1% increase according to the PHIN data.

In spite of the overall growth, compared to 2025 three English regions reported falls in the number of insured admissions using PMI. They were the East of England (0.7%), North East (0.2%) and the South East (3.1%), along with Northern Ireland (11.4%).

After witnessing a large rise (11%) in 2024, Northern Ireland’s percentage decrease was the largest of any nation or English region in 2025.

The largest rises for insured admissions in England came in the West Midlands (9.3%). Scotland had the next largest rise (5%).

By volume, the biggest increases were in London (4,870) and the West Midlands (3,190). The largest decrease came in the South East (3,790).

Self-pay continues to plateau

Self-pay admissions in 2025 were largely unchanged up just 0.2% or by 565 admissions compared to 2024, meaning this was just 85 admissions behind 2023, the record year so far.

Q1 and Q2 2025 were the two highest quarters ever for admissions by self-pay.

However despite this, admissions financed by self-pay fell in six English regions across the year.

The biggest percentage decrease was in the North West (4.1%). It increased in Scotland (7.2%), Wales (1.3%) and the East Midlands (7.9%), North East (5.3%) and West Midlands (6%).

The proportion of admissions by payment method stayed at 70:30 insured to self-pay.

Top 10 procedures

The Top 10 procedures in 2025 stayed the same as in 2024, although eight of them had fewer admissions than in 2024.

Upper GI endoscopy diagnostic and bladder examination via cystoscopy saw the biggest decline by volume of admissions (1,205). Bladder examination via cystoscopy also saw the biggest percentage decrease in admissions (10.4%).

Despite the overall growth in admissions in 2025, there were also large drops outside the Top 10 including weight loss surgery – gastrectomy (59%) and diagnostics – blood test (43%).

Cataract surgery continued as the most common reason to be admitted to a private hospital, but therapeutics – chemotherapy had the biggest admissions increase by volume (4,690) and percentage (6.3%) in the top 10 procedures.

PHIN noted that patients usually required multiple admissions for this treatment and the number of admissions they had varied depending on their health.

Outside the top 10 many procedures saw increases, including varicose vein sclerotherapy (54%), breast reduction (19%) and surgical treatment for endometriosis (12%).

While cataract surgery continued as the most popular procedure overall, it was only the third most popular for admissions funded by private medical insurance.

Therapeutics – chemotherapy ranked as the most popular with upper GI endoscopy – diagnostic and colonoscopy – diagnostic rounding out the top four.

The traditional big three of private admissions, cataract surgery, hip replacement (primary) and knee replacement (primary) remained the three most popular admissions for self-pay patients.

PHIN further noted that while insurance also paid for diagnostic procedures, the big difference from insured admissions came in the form of cosmetic surgeries.

Breast enlargement, breast implants and breast reduction all featured in the self-pay top 10.

Active consultants

The number of active consultants operating in the sector hit the highest ever in 2025 reaching nearly 13,400. This was 2.9% up on 2024.

The number of consultants active in private healthcare regularly fluctuates as new consultants start working in the private sector, and existing ones go on sabbatical, stop working privately, or retire.

While every private healthcare speciality in the top 10 saw an increase in consultants working in it, the largest volume and percentage increase in active consultants in the top 10 procedure groups in 2025 was in general surgery with an additional 382 consultants (16.8%).

General surgery also had the biggest increase in 2025. Trauma and orthopaedics remains the speciality with the most active consultants in the private sector.

Patient demographics

In terms of how people pay for treatment, there was an increased number of insured admissions for both sexes in 2025 compared to 2024.

Female insured funded admissions increased 0.6% and male admissions 1.0%.

There was an increase in admissions across most age groups, compared to 2024.

The largest volume increase was in the 60 to 69 age group (5,715) followed by the 40 to 49 age group (2,525). The largest percentage increase was in the 10-19 (5.3%) age group.

Private healthcare as proportion of English admissions

Despite this being another record year for private hospital and clinic admissions, the proportion of the total day-case and in-patient admissions conducted in the UK stayed the same.

The percentage of admissions funded by the NHS, but conducted in private hospitals and clinics, has also remained consistent over the past nine years, with a slight dip in 2020.

In 2025 the percentage of admissions in the NHS marked the highest since the pandemic, but was still slightly lower than pre-pandemic levels.