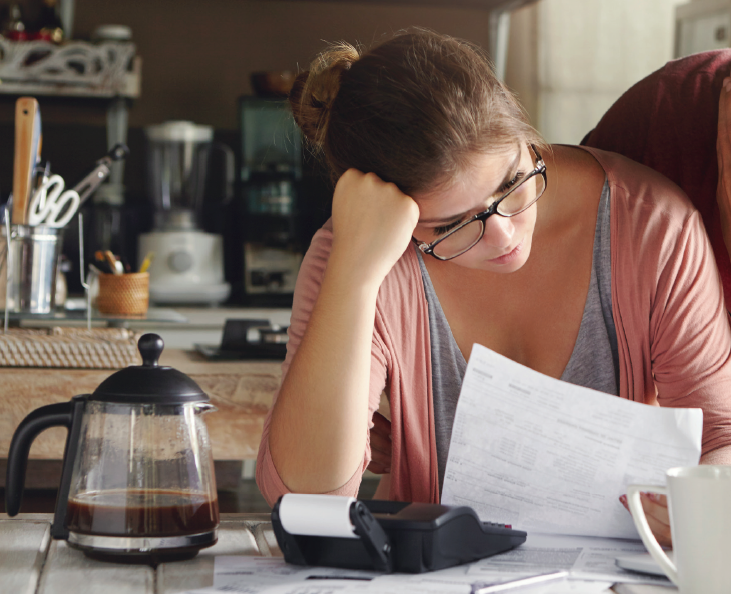

Spiralling inflation and energy costs have combined to create a cost of living crisis in which some people have been left with a choice between eating and heating. As a result, some customers are asking themselves whether the cover they have in place is essential?

But added value services are proving a potent weapon for advisers in changing that perception as products evolve and become more flexible to meet individual customer’s mental and physical wellbeing needs.

Employers are also seeking different methods and alternative benefits to support their workforce on limited budgets as higher prices bite.

And advisers should prepare themselves for a tough year as all of this seems increasingly necessary in an uncertain future where soaring costs seem baked-in for the remainder of 2023.

Cutting back on ‘non-essentials’

“The cost of living crisis means most households are scrutinising their spending habits,” Jennifer Gilchrist, protection specialist at Royal London, tells Health & Protection.

“The concern is that people’s motivation to protect themselves and their family financially from an unexpected life event has been forgotten along the way and their monthly premium is seen as a way of cutting back on outgoings.”

Debbie Kennedy, chief executive of LifeSearch, agrees – warning consumers have had to scrutinise spending more and find ways to cut back, particularly on items they consider ‘non-essential’.

“Our team of specialist advisers are on hand to have these conversations and guide consumers to stay protected,” Kennedy continues.

“For many clients, this has instigated a review of existing cover and where necessary, tailoring of insurances to meet budgets.

“During these reviews, advisers have been highlighting the support services attached to policies that include mental health and even money management guidance.

“Many insurers are now prepared to offer payment holidays for those struggling with their financial requirements, and advisers are helping to broker such agreements.”

LV= is one such insurer offering payment breaks, having continued the option on from its Covid-19 support interventions.

“In certain situations, those facing financial hardship and unable to pay their premiums are eligible for payment breaks that offer relief without sacrificing their cover,” says Mike Farrell, the mutual’s sales and marketing director.

“Payment breaks are offered a month at a time, for up to three months with no requirement for premiums to be repaid. Decisions are made on a case-by-case basis, subject to certain eligibility criteria.”

Employers equally feeling squeezed

But employers are equally feeling the squeeze, with Charlie Cousins, owner of Hooray Health & Protection revealing some group private medical insurance (PMI) customers are now choosing different payment schedules or alternative benefits to suit their budgets.

“We have seen clients making the switch to paying monthly rather than annually, giving people an opportunity for alternative options that are going to better fit with their financial needs,” he says.

“Insurers are now making this really easy to do and have shifted to no longer chasing payments so intensely.

“There has also been a rise in popularity for everyday benefits such as dental and optical cover. These are becoming a priority and increasingly sought after to help ease the burden each year.”

Health Shield research released at the end of last year revealed 81% of employees wanted to extend their workplace benefits to their whole family. And according to Katharine Moxham, spokesperson for trade body Group Risk Development (Grid), group protection customers are also increasingly seeking more bang for their buck.

“Where people and businesses are hurting financially it makes sense for employers to squeeze as much value as they can out of the benefits package,” she says.

“Since most group risk products come with a free employee assistance programme (EAP), the most obvious place to start is by signposting employees and line managers to the help and tips available on the EAP’s website as well as the more personal support the service can provide.”

This was echoed by Santé Group chief executive Paul Nugent, who notes that he has seen more emphasis on the use of integrated support services which are included in most financial products, including EAPs.

Other benefits such as retail discount schemes that provide cash back on shopping can really help with the increased costs, Nugent adds.

Importance of product flexibility

For Zurich UK director of retail protection Louise Colley, the cost-of-living crisis has been a “stark reminder” of the importance of product flexibility.

“Many households are feeling the squeeze and looking to make savings, but the financial protection provided by insurance is the last thing they can afford to lose,” Colley explains.

“Flexing cover down temporarily is better than losing it altogether, and products that allow this have come to the fore. Similarly, people don’t want to pay for product features they won’t use – for example, children’s cover for customers whose offspring have flown the nest.

“People want flexibility, but at the same time choice and value for money.”

In terms of the fresh thinking on offer, Debra Clark, head of specialist consulting at Towergate Health & Protection, revealed one area of development the firm has seen with providers is the integration of discount or cashback options as an added value part of their insurance proposition.

“This includes private medical insurers, cash plan providers and some of the group risk providers, as well as standalone solutions,” Clark continues.

“Some of these focus on purely health-related items or shops but others are broader. Anything that can be done to help people’s money go a bit further is a good thing.

“It is vital that companies make their employees aware of these benefits with regular communication, aimed carefully at the different demographics. This is something we would proactively support our clients with to ensure the highest rates of engagement,” she adds.

Joined-up wellbeing support

Miles Robinson, owner of Home Group Financial, notes protection providers are now offering discounts to fitness equipment, nutrition consultations and gym discounts in order to promote healthy-living in a more cost effective manner.

Robinson adds as the market becomes more competitive he expects there will be further improvements to customer-focused products.

Andrew Marchant, protection claims liaison manager and mental health first aider at Canada Life, says that with the cost of living potentially affecting multiple areas of an individual’s life – mental, physical, financial – the insurer is seeing more employers seeking a joined-up offering where wellbeing strategies link a variety of needs.

Backing up Marchant’s assertion, research from Vitality found 44% of UK workers would like their employers to do more to support their health and wellbeing needs.

As a result, the insurer said it was seeing an increasing amount of employers looking to offer a deeper level of support to their workforce.

The way in which these services are being delivered is also evolving with a particular shift over recent years in a virtual capacity, particularly as hybrid working has been increasingly adopted.

Matthew Reed, founder and managing director at Equipsme, says while not every business can respond to the crisis with blanket pay rises, he is seeing firms increasingly looking to rebalance their benefits strategy to offer better support that spans all three fronts of financial, mental and physical wellbeing.

And he adds these are being aimed at ‘shop floor’, where the cost-of-living crisis is biting the hardest.

This is because as Paul Chedzey, commercial director of WorkLife, points out the three components of wellbeing are interlinked.

“The extent of your financial wellbeing is determined by how you feel about your financial situation, not just by how much you have in the bank,” Chedzey says.

“Not feeling in control with enough money to meet your needs significantly impacts mental wellbeing. That not only impacts the individual wellbeing of employees, but also productivity.”

Cost increases largely baked in for 2023

Looking to the future, Rebecca Hill, head of marketing at Cirencester Friendly, predicts while the warmer spring weather, when it comes, will ease some pressures, particularly on energy costs, there is no sign of food prices coming back down any time soon.

“Many people will continue to find things tough and we are committed to going above and beyond to help our members when they need it,” she says.

“It is more important than ever to have the basics covered no matter what the future holds. We will be working hard with advisers to get this message across, letting more people know income protection is an affordable option to give them just that.”

And with Legal & General last week warning of a tough 2023 for protection in light of the cost of living crisis, Steve Herbert, wellbeing and benefits director at Partners&, expects that while inflation should start falling, prices are unlikely to follow suit just yet.

“The cost increases of the last 18 months are largely baked-in for 2023, and those prices will continue to rise in line with inflation and often above pay awards too,” Herbert says.

“It should also be noted that during the course of 2023 there are approximately 100,000 households each month leaving their very low-cost fixed-rate mortgage deals, and being exposed to mortgage rates which are much higher than they were during the pandemic.

“This will extend the cost-of-living crisis for many households even further. Yet even once the immediate crisis has subsided, the need for financial wellbeing support will remain.

“The truth is that UK living standards have been stagnating or decreasing ever since the financial crisis of 2008, and this is now a long-term issue for employers and employees to deal with,” he concludes.