Soaring numbers of high value claims which have more than trebled in frequency since the pandemic and a doubling of mental health support use are among the key causes of steeply rising medical insurance claims costs.

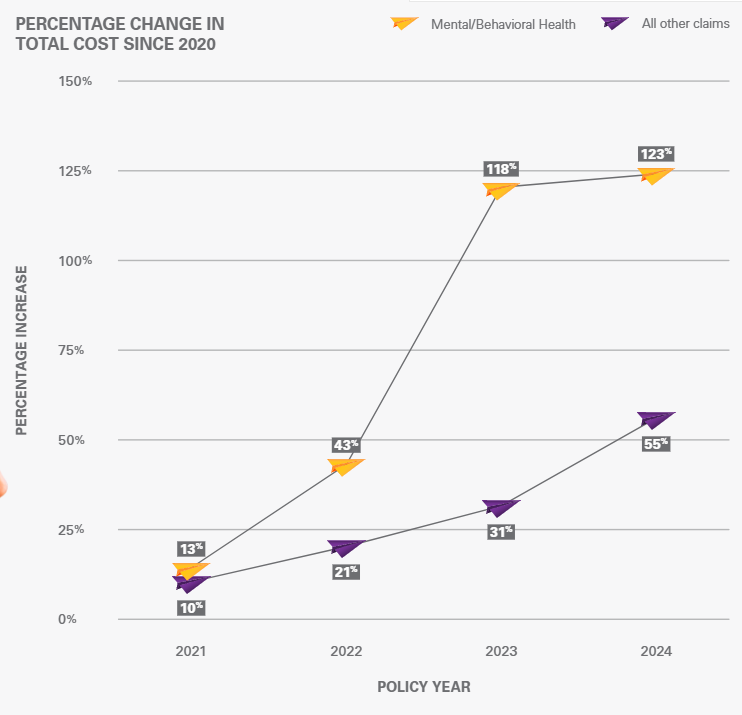

Insurer Tokio Marine’s annual market report for 2026 indicated a 123% increase in the cost of mental health claims since the start of the Covid pandemic.

It noted that while these claims did not represent a large portion of its stop loss claims, it has seen a sharp increase in their total cost, starting in 2022.

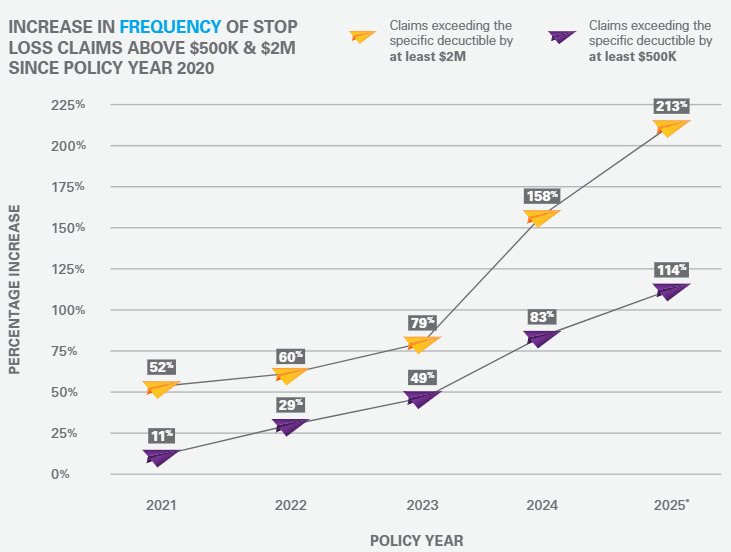

However, more notably claims of more than $2m have more than trebled in the six-year period triggering a significant effect in the insurance market.

Mental health claim frequency is cost driver

While the severity of mental health claims has increased since 2020, the primary contributory factor behind this increase in costs is frequency of claim.

Though costs continue to increase, the rate of increase has since slowed.

The authors suggested that Covid-19 had been a key factor behind the increasing frequency of these claims, along with growing awareness of various neurological disorders such as attention deficit hyperactivity disorder (ADHD), autism, and obsessive compulsive disorder (OCD), as well as a destigmatisation around mental health conditions in general.

Large claims up significantly

The report, which draws on six years of proprietary claims data, also found that claims above $2m had risen 213% since policy year 2020.

A significant factor behind this increase was the duration of the most complex cases.

The report noted that conditions leading to the largest claims were not only becoming more frequent, but also required sustained, intensive treatment that kept costs climbing long after the initial diagnosis or event.

Biggest driver of claims

Cancer continued as the single biggest driver of stop loss exposure, accounting for just over 35% of total paid claims and has grown as a share over the past four years as more advanced treatments are deployed.

Next came cardiovascular diseases at nearly 13% of all claims paid ahead of nervous system diseases in third (5.6%).

However, cancer and cardiovascular claims ranked well below those incurred for perinatal, neonatal and congenital or chromosomal abnormality categories where the claims exceed $1m, with plan members under the age of 10 making up 39% of all claims over $1m.

While perinatal/neonatal ranked only 7th in total costs, it accounted for the largest total paid out in 2025 – a claim of $8.93m.

Jay Ritchie, president and CEO of Tokio Marine HCC – accident and health group, explained the effects this was having for employer schemes.

“The market is tightening, pricing is becoming more disciplined, and deductible strategy plays an increasingly important role in how employers manage long-term risk,” he said.